India’s Digital Personal Data Protection Act (DPDP Act, 2023) is no longer a distant regulation. With rules expected to be notified and enforcement timelines firming up, financial institutions — NBFCs, banks, fintechs, insurers, and lending platforms — are under pressure to get their data handling practices in order.

If your business collects, processes, or stores customer personal data, this checklist is for you.

Who Needs to Comply With the DPDP Act?

The DPDP Act applies to any entity that processes digital personal data of individuals in India — whether the processing happens inside India or outside, if it involves offering goods or services to Indian data principals.

For financial institutions specifically, this captures:

- NBFCs and digital lenders processing borrower PAN, Aadhaar, bank statements, and income data.

- Fintechs and neo-banks running eKYC, video KYC, or app-based onboarding flows.

- Insurance companies collect health declarations, nominee details, and identity documents.

- Payment aggregators storing card, UPI, or wallet holder data.

- Compliance and RegTech platforms processing data on behalf of regulated entities.

If you collect, store, or share any personal data during customer onboarding or ongoing operations, the Act applies to you.

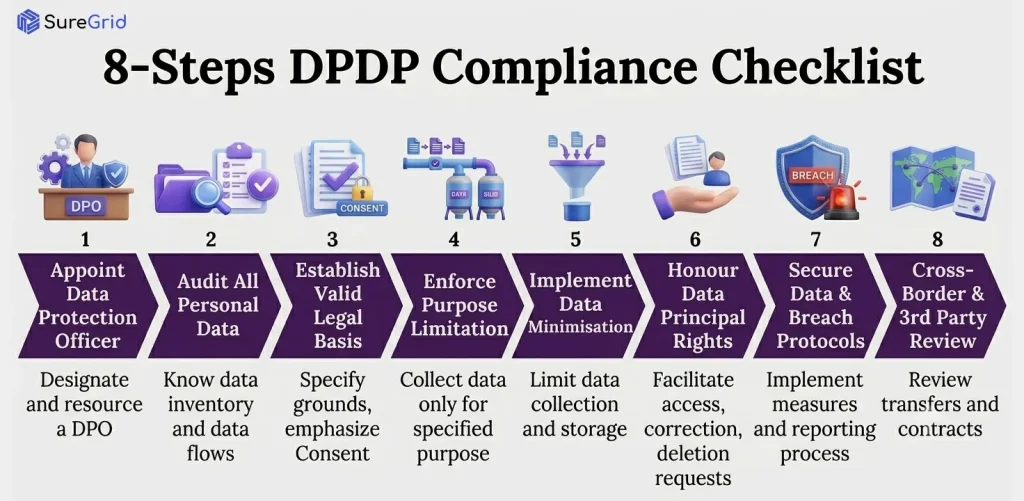

8-Steps DPDP Compliance Checklist

Step 1: Appoint a Data Protection Officer (if applicable)

Significant Data Fiduciaries — a category the government will designate by volume, sensitivity, and risk — must appoint a DPO. Even if your organisation falls below the threshold, it is prudent to assign clear internal ownership for data protection.

Action: Identify a responsible individual or team for DPDP compliance and document their mandate.

Step 2: Audit All Personal Data You Collect

Map every touchpoint where you collect personal data: onboarding forms, KYC APIs, third-party integrations, CRM systems, loan management platforms, and analytics tools.

Action: Build a data inventory that captures: what data is collected, why, where it is stored, who can access it, and for how long.

Simplify Your Compliance & Stay Audit-Ready

Help your team manage controls, risks, and audits with ease

Step 3: Establish a Valid Legal Basis — Starting With Consent

The DPDP Act requires a lawful basis for processing personal data. For most customer-facing workflows, this means free, informed, specific, and unambiguous consent from the data principal. Financial entities may also rely on legitimate uses defined under the Act (such as compliance with law or performance of a contract).

Action: Review your current consent mechanisms. Pre-ticked boxes, buried clauses, and bundled consent are not compliant. Build a clear consent notice that states the purpose in plain language.

Step 4: Define and Enforce Purpose Limitation

You can only use personal data for the purpose for which it was collected. Collecting a customer’s Aadhaar for KYC and then using it for marketing profiling would violate the Act.

Action: Tag every data field in your systems with an approved purpose. Restrict downstream access to only what is necessary for that purpose.

Step 5: Implement Data Minimisation

Collect only what is strictly necessary for the defined purpose. Excess data collection increases your DPDP liability and broadens your breach exposure.

Action: Review every data field in your onboarding and servicing flows. Drop anything that is not directly required. Preference verified data from regulated sources over raw document storage wherever possible.

Step 6: Honour Data Principal Rights

Under the DPDP Act, every individual has the right to:

- Access information about what data you hold on them

- Correct inaccurate data

- Erase their data (subject to legal retention obligations)

- Withdraw consent at any time

- Nominate a representative for these rights

Action: Build or procure a system to receive, track, and resolve data principal requests within the timelines specified in the rules. Train your customer support team to handle these requests correctly.

Step 7: Secure Personal Data and Establish Breach Protocols

The DPDP Act requires Data Fiduciaries to implement reasonable security safeguards. A personal data breach must be notified to the Data Protection Board and the affected data principal.

Action: Conduct a security review of all systems that hold personal data. Define a breach response SOP with clear escalation paths, timelines, and notification templates. Manual processes will not scale — this is where automated breach detection becomes critical.

Step 8: Review Cross-Border Data Transfers and Third-Party Contracts

If you share personal data with processors (cloud providers, API vendors, analytics platforms), you remain responsible as the Data Fiduciary. Data transfers to certain countries may be restricted under the rules.

Action: Audit all vendor contracts. Ensure Data Processing Agreements are in place. Restrict data transfers to jurisdictions permitted under the notified framework.

How SureComply Helps Financial Institutions Stay DPDP-Ready

Meeting the DPDP Act is not a one-time exercise. Regulations evolve, data flows change, and breaches can happen without warning. The institutions that stay compliant are those with continuous visibility — not those that ran a checklist once and moved on.

SureComply’s compliance automation platform is built for exactly this.

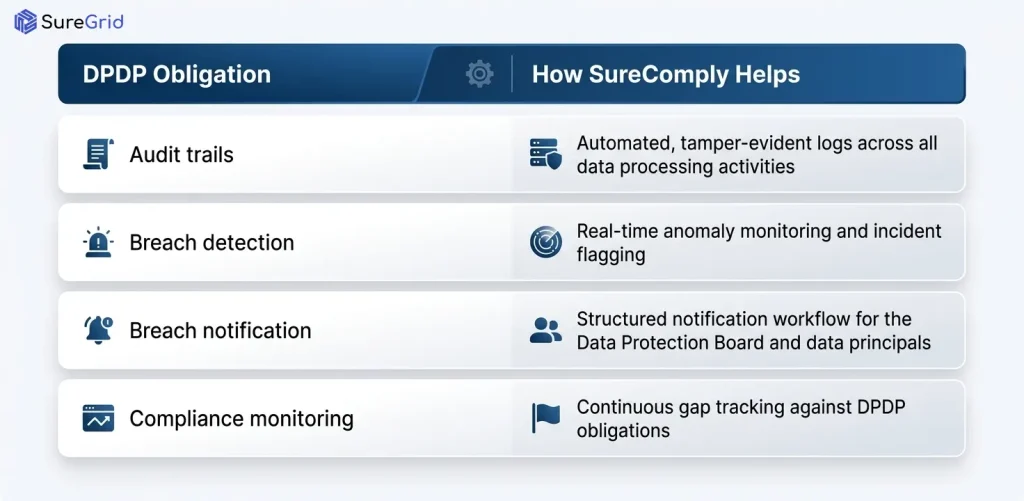

Audit Trails That Hold Up to Scrutiny

Every data processing action — who accessed what, when, and for what purpose — needs to be traceable. Under the DPDP Act, the burden of demonstrating compliance lies with the Data Fiduciary.

SureComply maintains automated, tamper-evident audit logs across your data workflows, giving you a clear record of every processing activity. When the Data Protection Board comes asking, your evidence is already organised.

Breach Detection and Notification Without the Scramble

The DPDP Act requires prompt notification to the Data Protection Board and affected data principals in the event of a breach. Getting this wrong — or getting it late — carries significant penalty risk.

SureComply’s breach monitoring continuously watches for anomalies across your data environment, flags potential incidents in real time, and supports your notification workflow so you are never scrambling to piece together what happened.

Continuous Compliance Monitoring

Regulatory requirements will be updated as the DPDP Rules are notified and refined. SureComply tracks the compliance status of your organisation against current obligations and flags gaps before they become violations.

Key Deadline and Milestone Table

| Milestone | Status / Expected Timeline |

| DPDP Act passed | August 2023 — enacted |

| DPDP Rules notified | Awaited; draft rules circulated in early 2025 |

| Enforcement and penalties | After rules are notified; grace period expected |

| Consent framework implementation | From rules notification date |

| Data Principal rights mechanism | From rules notification date |

| Significant Data Fiduciary designation | To be notified by MeitY |

| Data Protection Board operational | Post rules; appointments ongoing |

Note: Timelines above are based on publicly available information as of mid-2025 and may be updated when rules are formally notified. Follow MeitY announcements for the definitive schedule.

FAQs

Ques: Does the DPDP Act replace existing RBI KYC norms?

Ans: No. The DPDP Act operates alongside RBI’s Master Directions on KYC. Where the two overlap — such as on retention periods or consent — the more stringent obligation typically applies. RBI-regulated entities must comply with both frameworks simultaneously.

Ques: Do we need fresh consent from existing customers?

Ans: The Act’s approach to legacy data will be clarified in the final rules. The current expectation is that entities will need to obtain compliant consent from existing customers for any ongoing or future processing, particularly if the original consent did not meet the Act’s standards.

Ques: How long can we retain customer personal data?

Ans: Under RBI KYC norms, regulated entities must retain KYC records for at least five years after the end of the customer relationship. The DPDP Act requires that personal data be erased once the processing purpose is fulfilled. These obligations can be reconciled: retain data for the RBI-mandated period as a legitimate retention basis, then erase once that obligation lapses.

Ques: What qualifies as a personal data breach under the DPDP Act?

Ans: Any unauthorised access, disclosure, alteration, or destruction of personal data constitutes a breach. The DPDP Act requires notification to the Data Protection Board and affected data principals. The rules will specify timelines, but organisations should treat notification as a time-sensitive obligation and have a response plan in place before a breach occurs.

Ques: How does compliance automation reduce DPDP risk for financial institutions?

Ans: Manual compliance tracking breaks down at scale. Financial institutions process thousands of customer records daily, often across multiple systems and vendors. Compliance automation gives you continuous visibility into your data processing activities, flags anomalies before they escalate, and maintains the audit trail you need to demonstrate accountability to regulators. It converts DPDP compliance from a periodic exercise into an ongoing operational function.

Simplify Your Compliance & Stay Audit-Ready

Help your team manage controls, risks, and audits with ease

")

_ Key Components and How it works_")